Full Income Analysis: 59-year-old Couple Retires with $200k/year At A 6.4% Annual Tax Rate

(don’t forget to checkout the video of this case study too)

⭐️ Summary of important details ⭐️

✅John & Jessica are 59

✅ They want $200k/year of immediate retirement income

✅ They are also hoping for a tax-free retirement (or as close as possible)

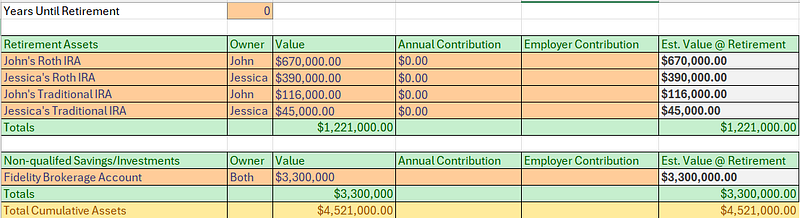

✅ They have $3.3M in a taxable brokerage investment account

✅ They have $167k in taxable IRA’s & $1.06M in Roth IRA’s

✅ They will get $4,000/month from Social Security at age 62

Retirement Goals:

✅ Comfortably stay retired, reduce tax liability as best as possible, and keep money working for you in retirement

✅ Preserve as much wealth as possible while comfortably generating $200,000 per year of retirement income

Traditional Retirement Income Planning = The 4% Rule

The 4% Rule states that if you keep your entire retirement balance invested in the market, approximately 50% in stocks and 50% in bonds, then you should be able to withdrawal 4% per year in annual income (and it’s very likely to last for 30 years although certainly not guaranteed).

It’s important to note that this is NOT a principal-protection strategy. It’s a safe withdrawal strategy that uses a low withdrawal rate as risk management for Retirement Income Planning.

Supplemental income following 4% rule = $4,521,000 x 4% = $180,840 per year (or $15,070 per month)

My Safe Money Retirement Income Philosophy:

My philosophy is to leverage a market-independent income source from an insurance company to allow for much higher income withdrawals while also increasing the safety of your retirement income plan by providing a streams of guaranteed, lifetime income that are not subject to market losses leading up to, or in retirement.

This provides more liquidity, more flexibility, and allows you to keep more wealth in the market, positioned for long-term growth.

Overview of 3 Safe Money Buckets (not including tax-free wealth transfer vehicles):

These vehicles can be used either for principal protection, for market-indexed growth (with no risk of loss), or as a way to maximize lifetime, retirement income

Safe Money Bucket #1: Guaranteed Rate Annuities

Principal protection + fixed, guaranteed growth

- Like CD’s, but typically a bit higher interest rate (issued by insurance companies)

- No annual 1099’s like CD’s (money can accumulate tax-deferred within these vehicles)

- Interest can be taken as income, or can be rolled back into the contract for compounded growth

Safe Money Bucket #2: Indexed, Growth Annuities

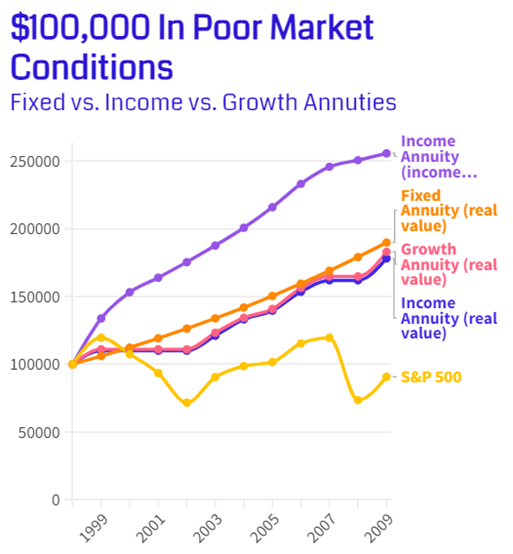

Principal protection + market-indexed growth (see chart below — growth annuity)

- Designed to beat CDs and fixed annuities (without risk of loss)

- Not designed to beat the stock market over the long haul

- Allows you to participate in the growth of the market with a segment of your portfolio with no risk of loss

- No annual fees

Safe Money Bucket #3: Indexed, Income-Focused Annuities

Principal protection + Guaranteed Lifetime Income + Market-indexed Growth (see chart below — income value + real value)

- Designed to accumulate maximum income value (often growing at 10% per year or more)

- Still allows for market participation (like bucket #2) with no risk of loss

- Since these are income-focused the income is designed to grow faster than the real value of the annuity

- Provides a lifetime income guarantee (even if the value of the contract reaches $0)

Market-Independent Income-Maximization Strategy

This helps significantly increase our income withdrawals (beyond 4% annually) while simultaneously increasing the safety of our overall Retirement Income Plan

Key points:

- Not susceptible to market fluctuations leading up to retirement

- Income always unaffected by fluctuations in the market

- Generates 80% more income than you can from the market with the 4% rule (7.2% immediate payout for life OR we can allow it to continue growing )

- Eliminates the possibility of running out of money in retirement (guaranteed lifetime income)

- Allows more freedom & flexibility with remaining assets

- You (and your beneficiaries) always own 100% of the value of this contract

Retirement Income Analysis

Retirement Income Analysis Overview

- Total Retirement assets = $4,521,000

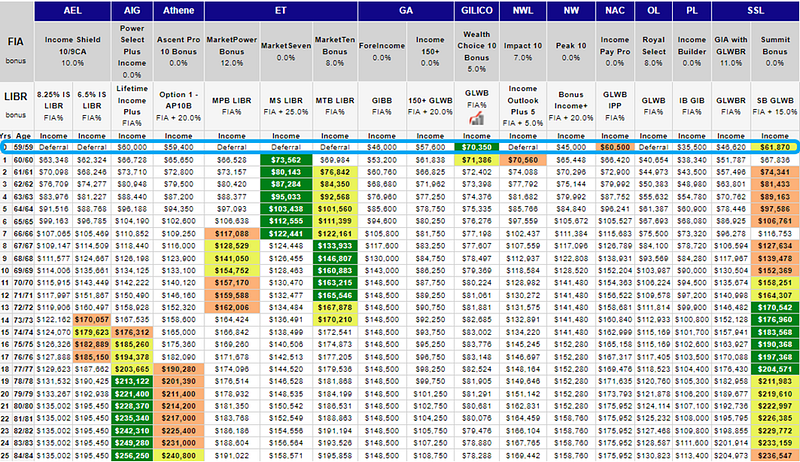

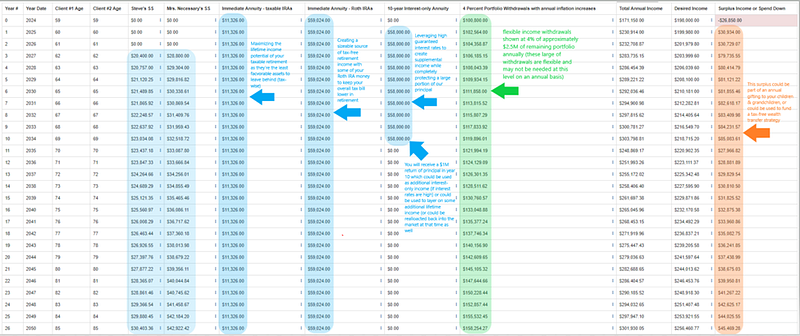

- $1,000,000 Allocated to Income-focused Annuity to provide $70,000+ per year of guaranteed, lifetime income (approximately 16% from taxable retirement accounts and the remaining from tax-free, Roth IRA accounts)

- $1,000,000 allocated to 10-year, guaranteed rate annuity at approximately 5.8% per year (providing 100% principal-protection & 45% more income than we can safely withdraw from the market at 4% per year)

- $2,521,000 will remain invested in the market (which we can very safely withdraw 4% per year from as supplemental income = approximately $100,840 per year adjusted for inflation annually)

- Withdrawals can be taken at greater than 4% per year based on the performance of the market (which we will review annually)

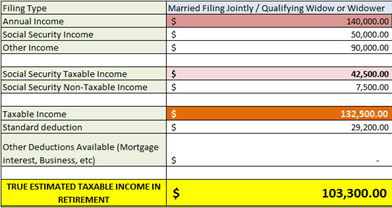

Estimated Tax Bill in Retirement

Estimated total annual income = $200k

minus ($60,000) of tax-free income from Roth IRA Annuity will not be considered taxable income (ever)

minus (36,700) of tax-free income collected via standard deduction & social security tax benefits

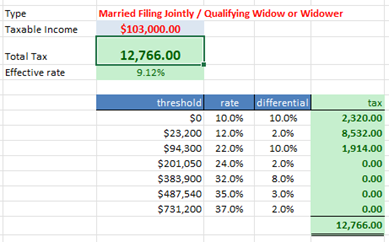

True Taxable Income = $103,000 (see below)

Estimated Total Annual Federal Tax Bill

$12,766 divided by a total of $200,000 of income

= 6.4% per year annual federal tax bill (+ state taxes if applicable)

My Retirement Income Recommendations:

- $1,000,000 to (2) indexed, income annuities based on Retirement Income Analysis ($161k from taxable retirement accounts + $839k from Roth accounts)

- $1,000,000 into 10-year, guaranteed rate annuity at 5.8% for short-term income + principal protection

- Remaining Roth IRA assets invested aggressively for long-term growth

Connect With Me & Access All My Resources Here

Enjoy this blog? You’ll probably enjoy this one as well: The 2 Most Important Targets for Determining Your Retirement Income Number

PS: I have an automated platform that allows you to shop for simplified life insurance solutions (on your own) including FREE estate planning tools

To your success,

Matt

0 Comments