How 3 Consecutive 10% Losses Can Destroy Your Retirement Income Plan ⚠️

(don’t forget to checkout the video of this blog too)

If you’re approaching retirement, there’s one silent risk that could quietly unravel everything you’ve built:

It’s not just about how much your portfolio earns — it’s about when those gains or losses occur.

Why the First Few Years of Retirement Matter So Much

During your working years, market volatility can be your friend.

You invest consistently, buy during dips, and let time smooth out the ride.

But once you begin taking withdrawals? The game changes. Dramatically.

Let’s walk through a simplified — but eye-opening — example…

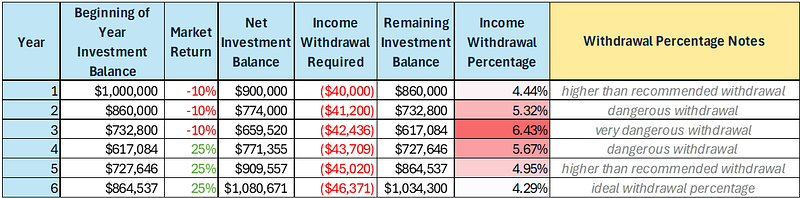

🔍 The $1,000,000 Portfolio Example

Imagine you’re retiring with a $1,000,000 portfolio.

You plan to withdraw a conservative 4% annually (adjusted for inflation), giving you $40,000/year of income.

But what if the market doesn’t cooperate?

Let’s assume a 3-year down market at the start of your retirement:

- Year 1: -10% market return

- Year 2: -10% market return

- Year 3: -10% market return

And remember, you’re still withdrawing an inflation-adjusted $40,000 annually, so your principal is being eroded away much quicker (see chart below).

📉 What Happens After Just 3 Down Years?

Your portfolio isn’t just losing value due to market losses — you’re also pulling money out.

After those first three years, you’ve lost a staggering 38% of your total portfolio value.

So now you’re left with just $617,084…

But your income need hasn’t changed.

To maintain your $40,000/year lifestyle, you now have to withdraw over 6% per year — a far less sustainable strategy.

Note: you would also need to achieve almost 25% per year in growth in years 4–6 (while taking income withdrawals) just to get your portfolio back to even at the end of year 6, so you could get yourself back to a safe, sustainable withdrawal rate of about 4% per year. To do this, would most certainly require a significant amount of market risk (which most retirees are trying to avoid).

You’re Left With 3 Bad Choices:

- Slash your income and lifestyle to preserve capital

- Increase market risk in hopes of making up for losses

- Risk depleting your assets and relying solely on Social Security

None of these are attractive options — and none are part of the plan you worked so hard to build.

✅ The Smart Move: Protect Part of Your Portfolio

This is why I’m a strong advocate for shielding a portion of your retirement portfolio — especially in the years leading up to and through early retirement.

One of the most effective tools?

The right kind of income annuity.

It removes market risk from your income stream during the years where losses could be most devastating.

And just as importantly:

- It provides guaranteed lifetime income

- It frees up the rest of your portfolio to stay invested for long-term growth

- It gives you the confidence to retire — even in uncertain markets

Final Thought

Don’t let bad timing derail your entire retirement.

Sequence of return risk is real — and potentially irreversible.

But with the right strategy in place, you can retire confidently with a predictable income floor and real upside potential.

Connect With Me & Access All My Resources Here

Enjoy this blog? You’ll probably enjoy this one as well: How This 59-Year-Old Couple Locked in $8k/Month of Guaranteed Income — While Still Building Wealth

P.S. Make sure you checkout my new one-page Long-term Care guide.

To your success,

Matt

0 Comments