How Much Can a 60 & 61-Year-Old Couple Really Collect from an Annuity? (starting in 5 years)🤔

💾 Make sure to save this post and watch the video of this blog too — it could be your roadmap to reliable retirement income. 💾

Meet Julie and Gus.

They’re 60 and 61 years old, planning to retire in five years. Like many, they’re looking for safety, predictability, and peace of mind in retirement.

Here’s a snapshot of their financial picture:

✅ $500,000 in a 401(k)

✅ $750,000 in a taxable investment account

✅ $5,600/month expected from Social Security starting in 5 years

Now let’s answer the big question:

“How much guaranteed income can they create — for life — using an annuity?”

Step 1: Lock In Lifetime Income with a Deferred Income Annuity

Julie and Gus decide to move their $500,000 from the 401(k) into a deferred income annuity (DIA). This type of annuity allows them to delay income for 5 years while locking in higher payouts for life.

After shopping the market and finding the highest paying guaranteed option, the numbers look like this:

🔒 Annual Guaranteed Income (starting in 5 years): $49,980

🔒 Monthly Social Security (combined): $5,600

📈 Total Monthly Income (Guaranteed for Life): $9,765

That’s $117,180 per year of fixed, dependable income.

With their investment account untouched, they now have flexibility for additional spending, unexpected expenses, or legacy goals.

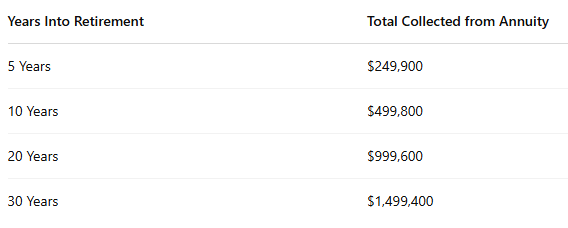

But How Much Do They Actually Collect from the Annuity Over Time?

Let’s break it down:

🔥 After 10 years, they’ve collected everything they put in

🔥 After 20 years, they’ve received twice their investment

🔥 After 30 years, they’ve taken out three times their investment

And here’s the kicker:

Even after 30 years, the income doesn’t stop. If one of them lives to 100, that $49,980 per year just keeps coming — for life.

“But What Happens If They Die Early?”

Great question — and a common concern.

Many people assume annuities are “use it or lose it”… but that’s not the case here.

Julie and Gus selected an income annuity with a death benefit, which means:

If they pass away before receiving the full value of their investment, the remaining value or payments will go to their beneficiaries.

So whether they live 5 years or 35 years past retirement, they know their money is never lost.

Final Thoughts 💬

Julie and Gus now have:

✅ Peace of mind

✅ Predictable income

✅ Control over their investments

✅ A legacy plan in place

This is what I call retirement income done right.

Want to run the numbers for your own situation?

Let’s chat. 😎

Connect With Me & Access All My Resources Here

Enjoy this blog? You’ll probably enjoy this one as well: 5 Powerful Ways to Build A Tax-free Retirement Income Strategy

PS: I have an automated platform that allows you to shop for simplified life insurance solutions (on your own) including FREE estate planning tools

To your success,

Matt

0 Comments