How to Boost Your Retirement Portfolio Income by 37.5% — With This One Simple Strategy💰

(don’t forget to checkout the video of this blog too)

When most people think about retirement, one word comes to mind: stability.

After decades of saving, the last thing you want is a retirement plan that feels like a rollercoaster.

That’s why fixed income sources — pensions, Social Security, and annuities — are so valuable.

They provide predictable, reliable income no matter what the market is doing.

But here’s a question worth asking:

👉 Should all of your retirement income come from these sources?

The answer is no.

While predictability is crucial, you still need some exposure to market growth if you want your income to keep pace with inflation and last for decades.

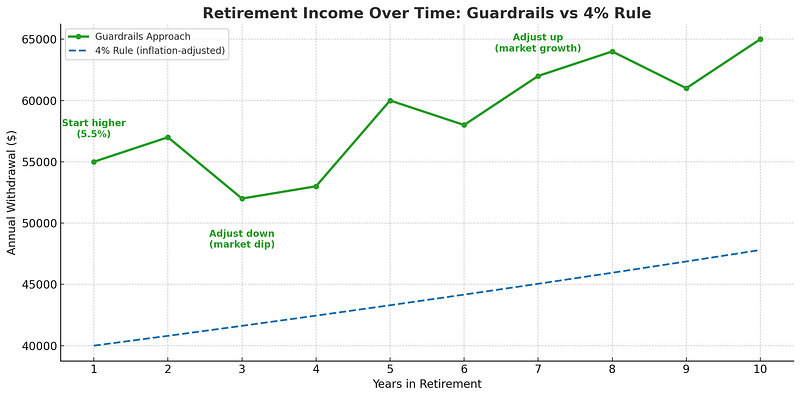

Why the “4% Rule” Falls Short

For years, the “4% Rule” has been the gold standard in retirement planning.

The rule says you can safely withdraw 4% of your portfolio each year, adjust for inflation, and your money should last 30 years.

Sounds simple.

But here’s the catch:

- It was designed to preserve assets, not maximize income.

- It assumes a rigid withdrawal pattern — the same inflation-adjusted withdrawal year after year, no matter what markets are doing (which requires a lot of discipline in down markets).

- It often leaves retirees underspending in their healthiest years because they’re afraid of running out of money later.

In other words, the 4% Rule is too conservative for many retirees.

The Guardrails Approach: A Smarter Way to Spend

What if you could safely withdraw 5.5% instead of 4% — a 37.5% boost to your income — while still protecting your portfolio?

That’s where portfolio guardrails come in.

This strategy builds flexibility into your retirement income plan by adjusting withdrawals based on market performance:

- Lower Guardrail: If your portfolio drops by 10–20%, you reduce withdrawals slightly.

- Upper Guardrail: If your portfolio grows significantly, you increase withdrawals to enjoy more lifestyle spending.

Instead of guessing the market, you’re simply adapting to it.

Why This Works

By setting guardrails, you give yourself permission to spend more in good years and automatically protect yourself in bad years.

This means you can:

✅ Enjoy more income in your early, active years (travel, hobbies, family experiences)

✅ Shield your nest egg during downturns by pulling back temporarily

✅ Maximize lifetime income, not just preserve assets

In practice, this flexible approach allows retirees to safely withdraw 5.5% or more — compared to the rigid 4% Rule — without meaningfully increasing the risk of running out of money.

Real-Life Retirement Isn’t Static

The truth is, retirement doesn’t happen on a spreadsheet.

Expenses fluctuate, markets rise and fall, and your lifestyle evolves over time.

That’s why static rules like “always withdraw 4%” don’t reflect reality.

Guardrails give you a dynamic, adaptable plan that works in the real world.

It’s not about predicting the market.

It’s about building a system that adapts with it — so you can spend confidently without second-guessing every withdrawal.

Final Thoughts

If you want to increase your retirement income by 37.5% without taking on additional market risk, consider moving beyond the 4% Rule and implementing portfolio guardrails.

This strategy gives you the best of both worlds: higher income in the years you want to enjoy it most, and the peace of mind that your nest egg can weather downturns.

Want help designing a retirement income plan that works in real life — not just on paper?

Connect With Me & Access All My Resources Here

Enjoy this blog? You’ll probably enjoy this one as well: 59-year-old Couple Converts $800k IRA into $1.6M Tax-free Roth — With No Market Risk & No Fees

P.S. Make sure you checkout my new one-page Long-term Care guide.

To your success,

Matt

0 Comments