How To Give Your Children $1.8M of Tax-Free Retirement Money (for only $291/month)

Don’t forget to checkout the video of this blog when you’re done reading).

You can give your kids a huge leg-up in the world by making a few smart and strategic decisions early in their life (just like my friend’s grandpa, which I talked about here).

This is just how wealthy people think; they think 2–3 generations ahead and how to position their entire family for future opportunities.

Here’s a perfect example of how to do that for your own children for a very nominal amount of money:

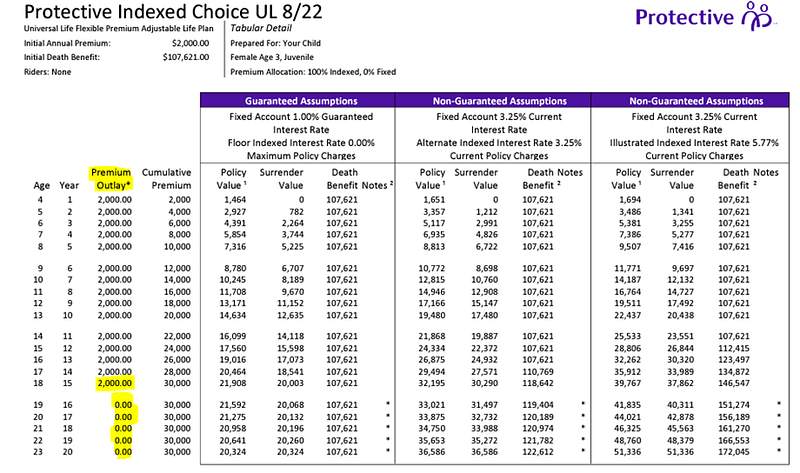

STEP 1 — $2000 per year into an IUL (geared to accumulate cash)

At age 3 you open an indexed universal life policy for your child, and you contribute $2000/year ($166/month) to that policy for 15 years (until your child is 18 years old).

At this point you will never then never put another dollar into that contract (highlighted in chart below).

This policy will give you an immediate $107,621 of insurance coverage (this is the minimum amount required in this example so that we can maximize the cash accumulation potential and keep the policy cost as low as possible).

At your child’s age 18 you can see above that they have about $40,000 of cash value that they can access ANY TIME completely tax and penalty-free (this illustration is shown conservatively at a 5.77% but historically, indexed universal life policies have averaged over 7% per year for the past 20 years)

The cash will continue to grow uninterrupted even when you pull money out of the contract (this is one of the main features that make these types of contracts so powerful from a tax and flexibility standpoint).

This policy can be used for anything (buying a house, starting a business, paying for education, taking a loan from yourself for a new car… the possibilities are endless).

It also fits all the safe money criteria that I talk about frequently, because the account will grow when the market does well, but the money is contractually guaranteed not to go backwards when the market doesn’t do well (that means the if the market drops 20% you don’t lose a dime).

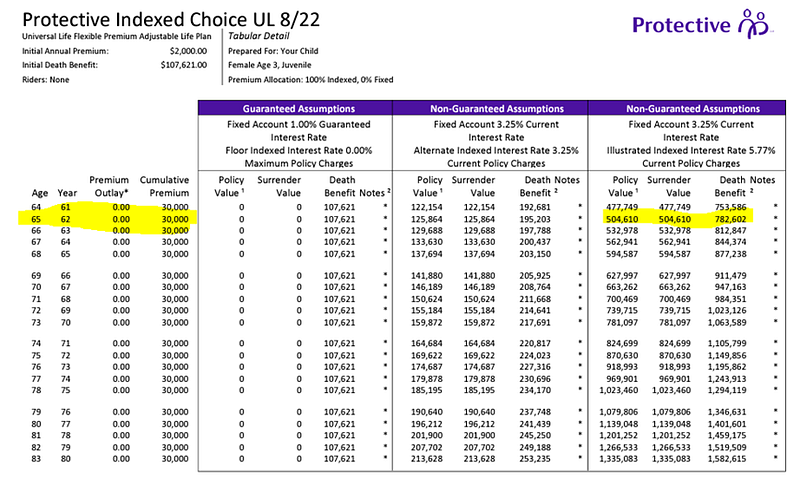

This policy will continue to grow (even though you’re no longer funding it) and by the time your child is 65 there will be approximately $504,000 in cash value and $782,000 in death benefit available to them (as seen below):

STEP 2 — $1500 per year into a 529 (shooting to have $35,000 at age 18 to transfer to a Roth IRA)

At age 3 you also put $1500/year ($125/month) into a 529 plan (based on the new law I just talked about in this blog)!

If you can accumulate money at just over 4% per year until your child turns 18, you will have about $35,000 which you can roll from the 529 Plan straight into a Roth IRA (tax and penalty-free).

At this point, you can invest the money a little bit more aggressively inside of the Roth IRA and if you’re able to earn approximately 8% per year until your child is 65, they will have approximately $1.3M in that account as well (and remember, this calculation is based on NOT CONTRIBUTING any money past age 18… if your child is able to max out their Roth IRA every year when they start working, which they should, these numbers will be a LOT higher!)

So if you total these 2 accounts up, you child will have $504,000 of safe money inside of the indexed universal policy that they can use however, and whenever they want, PLUS they will have about $1.3M dollars inside of a Roth IRA.

Leaving them with a total of $1.8M at age 65.

The best part is that every single dollar pulled out of BOTH contracts will be completely tax-free in retirement AND can be used to create a guaranteed, lifetime income source for them and their future family.

Also, money pulled out of BOTH of these contracts will not be considered provisional income….

Remember, provisional income is the determining factor for how social security is taxed, so if your kids are pulling money out of these 2 accounts they will have no provisional income and can therefore collect their social security check completely tax-free in retirement as well!

And you can do all of this for your children for just $291/month.

Like this blog? You can support my writing (and other great writers) for just a few bucks here & in the meantime, check this blog out: Leverage For Income + Leverage For Growth (a 2+2=5 scenario)

Let’s Chat:

Schedule Some Time Here

Let’s Connect:

Facebook | Instagram | YouTube | TikTok

Additional Resources:

Website | My Testimonials | Free Safe Money Book | Personal Development Resources

0 Comments