Your Returns Matter MORE When You Start Taking Income in Retirement (the sequence-of-return risk)

(Checkout the video of this blog too)

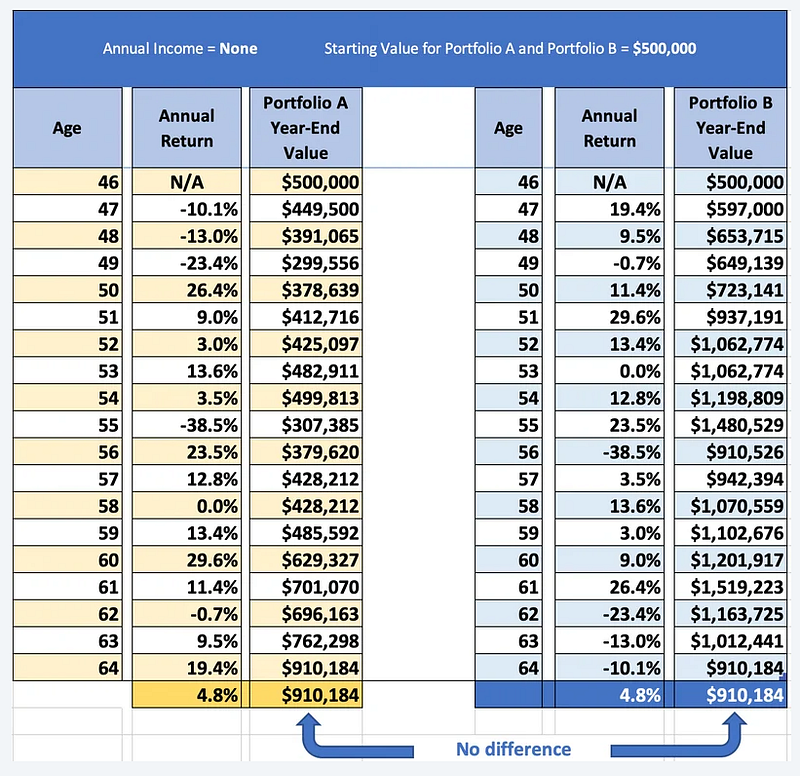

When you’re saving for retirement, it doesn’t really matter WHEN you get good returns or when you get bad ones.

Over time, the returns of a portfolio average out (if the average return is the same as seen below).

But when you start taking income out of your portfolio everything changes…

This is when the TIMING of your returns matter the most.

In fact, this is one of the biggest risks retirees face (and most are unaware of it).

You see, most money managers will tell you what your “average return” will “likely” be… especially in retirement.

In fact, a couple of months ago an investment guy told my father that he would be able to get him “8% per year throughout his retirement in the market AND provide a 6% withdrawal rate” (these are outrageously high numbers that would require a raging bull market for 30 years, but I digress).

I asked my dad, “well when does he plan on getting you the higher returns, and when does he plan on getting you the lower ones?”

Obviously, this is a bit of a facetious question, but it’s a very important question (and money managers cannot answer it because nobody knows what the market is going to do).

The average returns that most money managers promise are NOT the actual returns you will take home once you start taking income out of your retirement portfolio.

This is a key point that people approaching retirement must understand.

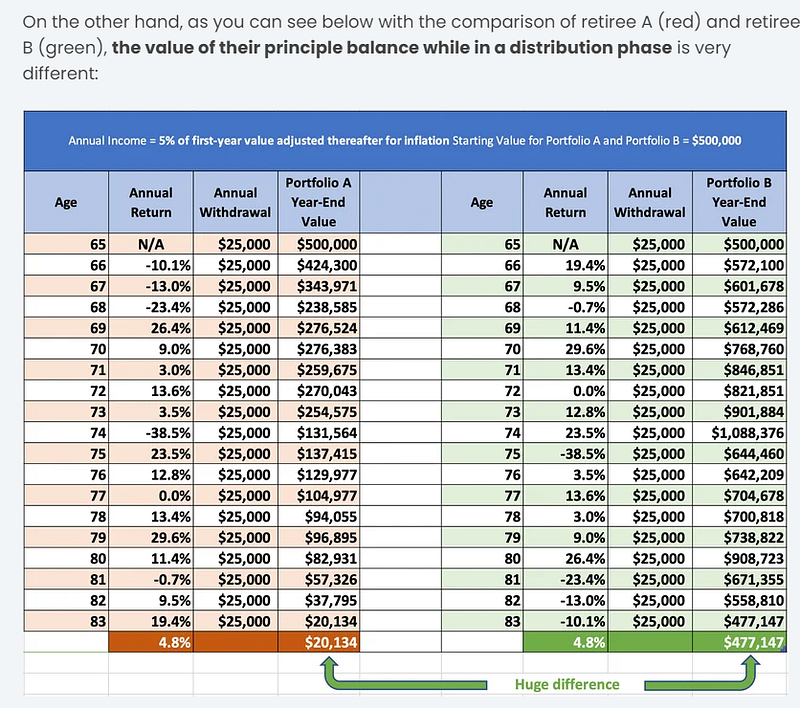

If the market drops in the early years of your retirement, you are MUCH more likely to run out of money in retirement. 😦

This is what’s called the sequence-of-return risk and it can very negatively affect your retirement income (see the example below)!

The best way to alleviate this risk from your portfolio is to create guaranteed income sources that are NOT dependent on the market (in addition to your pension and/or social security income).

This gives you complete protection against the sequence-of-return risk because you are transferring that to a company built to absorb the volatility of the market.

I’ve talked about this before, but creating an income floor (or a guaranteed, retirement income that covers your basic expenses in retirement) allows you to take the money that you are NOT using to create income to GROW in the market (since you can invest more aggressively when your retirement income is accounted for).

Because markets are good at GROWING your money, but because of the sequence-of-returns they are not effective at providing retirement income.

That doesn’t mean you shouldn’t utilize them because you absolutely should.

You just want your mentality in retirement to be simple…

Designate some of your retirement money for INCOME and designate the rest for GROWTH & flexible spending in retirement. 🤝

Let’s chat 💬😎

Connect With Me & Access All My Resources Here

Enjoy these blogs? You can support my writing (and other great writers) for just a few bucks here if you feel inclined, but be sure to checkout this blog in the meantime: 5 Reasons It Might Be A Bad Idea To Take Social Security Early!

To your success,

Matt

0 Comments